My name is Tony Dean and this is my blog on health, medicine and insurance.

I have worked in this industry for many years and have a lot of expertise on many issues related to health care, pharmacies and insurance.

This site is my hobby as well as an attempt to share my experience and knowledge and to be useful to someone, I thought long and hard about this idea and started in 2022.

I really hope that my articles will be useful to you, good luck!

Health Care in the USA 2022

Survey Highlights

- Forty-three percent of working-age adults were inadequately insured in 2022. These individuals were uninsured (9%), had a gap in coverage over the past year (11%), or were insured all year but were underinsured, meaning that their coverage didn’t provide them with affordable access to health care (23%).

- Twenty-nine percent of people with employer coverage and 44 percent of those with coverage purchased through the individual market and marketplaces were underinsured.

- Forty-six percent of respondents said they had skipped or delayed care because of the cost, and 42 percent said they had problems paying medical bills or were paying off medical debt.

- Half (49%) said they would be unable to pay for an unexpected $1,000 medical bill within 30 days, including 68 percent of adults with low income, 69 percent of Black adults, and 63 percent of Latinx/Hispanic adults.

- Sixty-eight percent of Democrats, 55 percent of Independents, and 46 percent of Republicans said President Biden and Congress should make health care costs a top priority in the coming year.

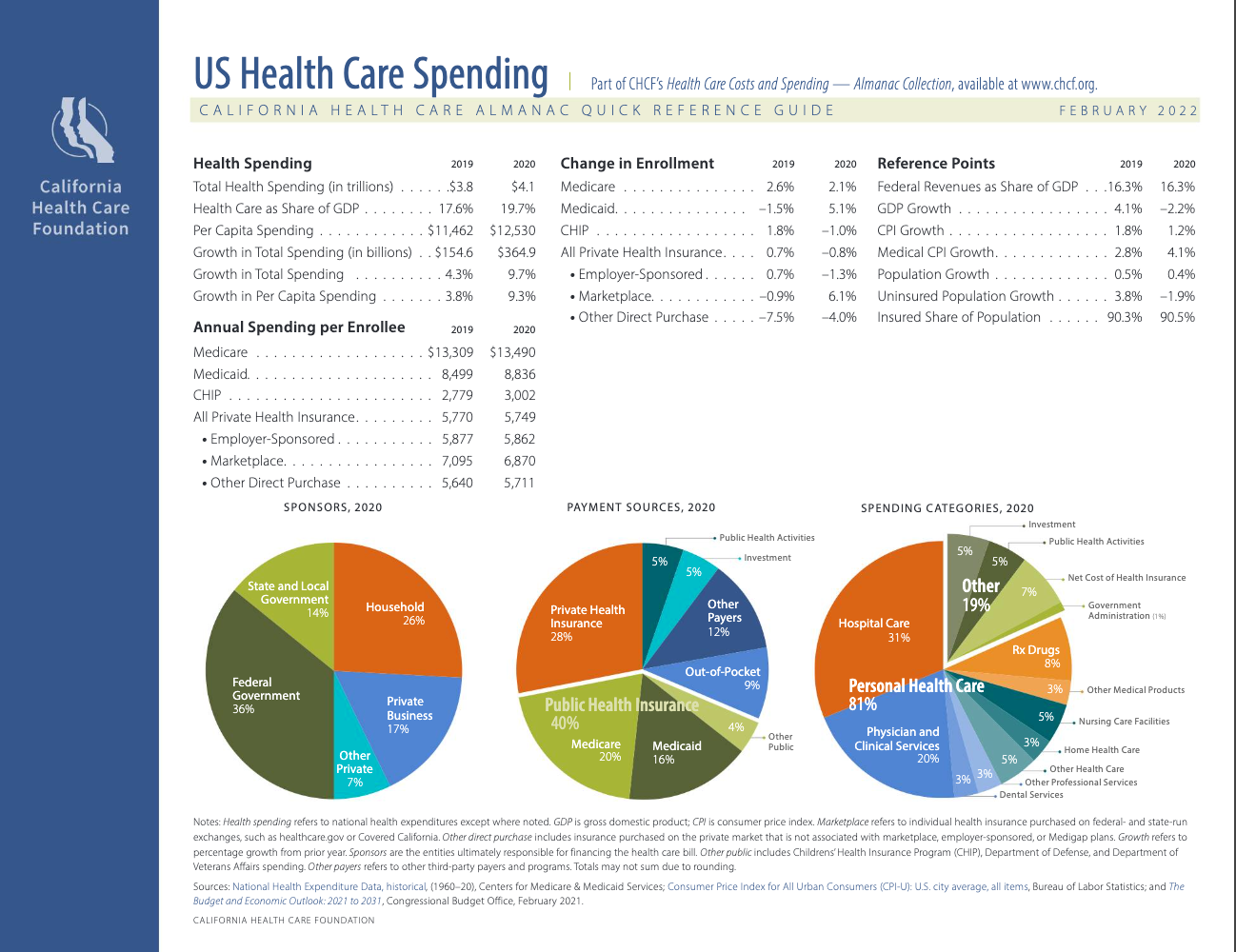

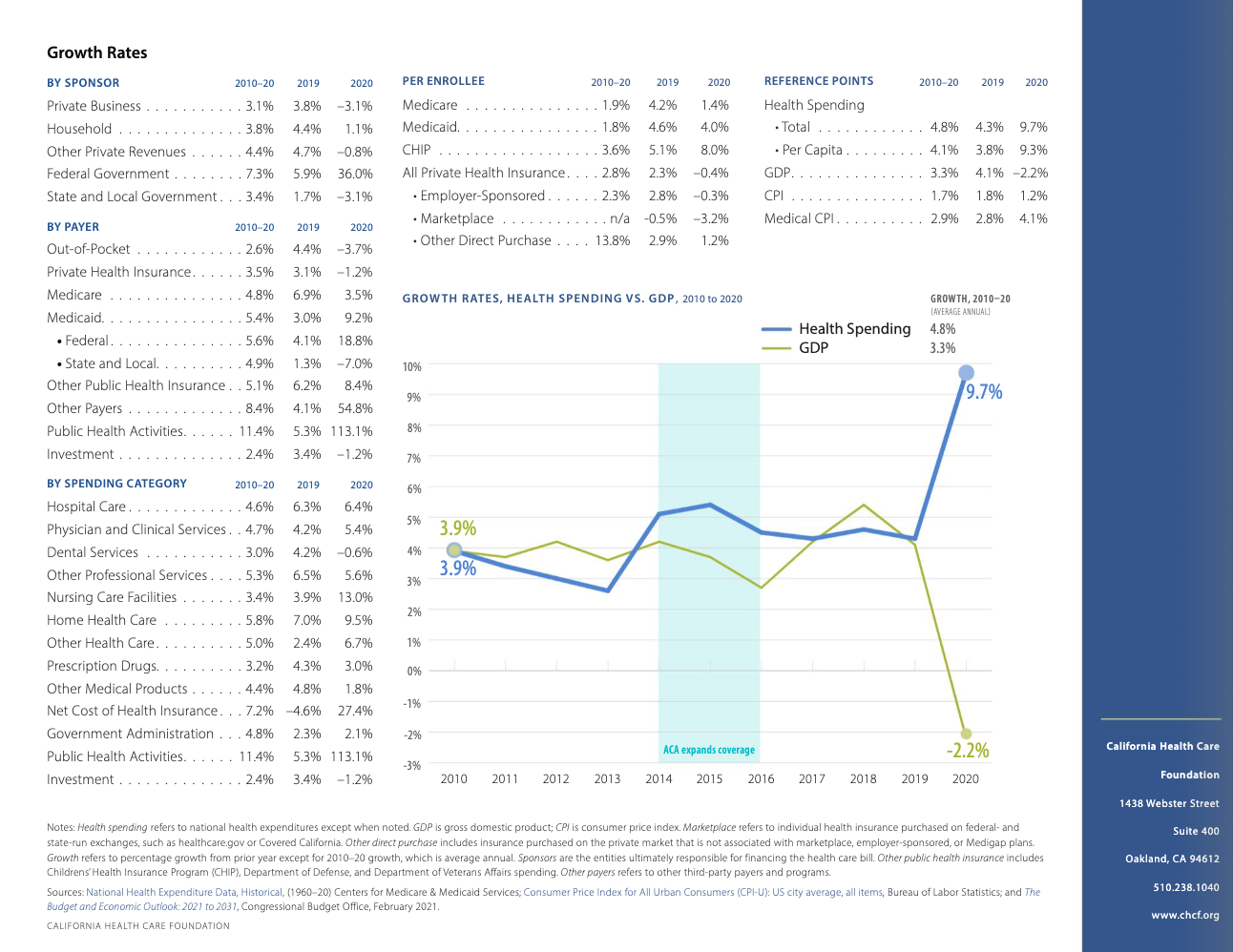

The bottom line for 2020

National health spending in 2020 increased 9.7% from 2019 to $4.1 trillion. The increase was largely driven by increases in federal spending during the COVID-19 pandemic. Excluding federal public health and other federal program spending, national expenditures increased just 1.9% in 2020 after an increase of 4.3 percent in 2019. A 2.2% reduction in GDP raised health care’s share of the economy to 19.7%, up from 17.6% in 2019. Health care spending averaged $12,530 per person, up from $11,462 in 2019.